In simple words, GSTR 2A (goods & services tax returns) is a monthly tax report with the detailed purchase of goods & services. GSTR 2A is a purchase-related certificate that each GST-registered firm receives through the GST site. It is a tax return that is generated automatically for each and every taxpayer. Since its launch in India in 2017, the Goods & Services Tax has greatly simplified the indirect taxes process.

If you are a registered taxpayer and submit your returns online through the GST site, the information will be stored and made available for future GST filings.

It is a read-only report that is used to give information on the taxpayer's purchase transactions.

How is GSTR 2A generated?

The following returns will automatically create GSTR 2A:

|

GST Returns |

Filed by |

|

GSTR 1 |

Regular registered seller/vendor |

|

GSTR 5 |

Non-resident |

|

GSTR 6 |

ISD (Input Service Distributor) |

|

GSTR 7 |

TDS Deductors |

|

GSTR 8 |

Operators in the E-commerce Industry |

Listed below are some points where GSTR 2A is generated

- If you are a seller (registered resident) who completes the GSTR 1 Form with transaction details

- When the Input Service Distributor submits the GSTR 6 Form

- If you're a non-resident seller who fills out the GSTR 5 Form with transaction information

- If a counterparty submits the GSTR 7 and 8 Forms, making sure to include the TDS and TCS information

How do I File Goods & service tax returns (GSTR 2A)?

You don't need to file it because it's a read-only document. It's auto-populated from other forms.

If an organisation discovers any inconsistency in the invoice details that its seller supplied in GSTR 1, you must accept, reject, alter, or defer its acceptance.

If any of the information needs to be changed, you must do so in GSTR 2 and the deadline is between the 11th and 15th of the month after the GST return is filed.

GSTR-2A format in detail

GSTIN - The dealer's GSTIN will be displayed here

a. Taxpayer's Name - The taxpayer's name, including their legal and business names

b. Month & Year - This section will list the month & year for which GSTR 2A is being filed

Also Read: Types of GST in India - What is CGST, SGST and IGST?

Part A, Part B and Part C of GSTR 2A are the Three Components

Part A

1. A registered person's inward supplies except for the supplies that attract reverse charge:

The majority of the information about purchases from sellers will be displayed in this area from the seller's GSTR-1.

The essential information, such as the rate, the GST amount, type, and the applicable ITC and ITC amount, will be listed here. This will not, however, include purchases made with a reverse charge.

The format is as follows:

2. Inward supplies from a registered user on which reverse charge tax must be paid:

This will include all purchases and supplies (both taxable and non-taxable) for which you will be required to pay GST under the reverse charge method.

The format is as follows:

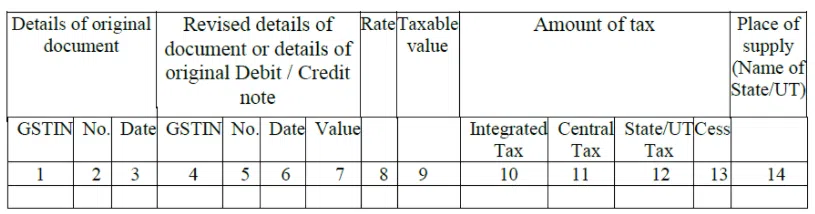

3. Receipts of debit/credit notes (including modifications) during the current tax period:

The data of debit and credit notes issued by the vendors during the month will be reflected in this section. It will also include any modifications discovered through a comparison of the revised and original papers.

The format is as follows:

Part B

1. The ISD credit (including modifications) received can be found in component B:

If you're a branch, the data in this part will be auto-populated for the same month if your head office files a GSTR 6 return.

The format is as follows:

Part C

1. TDS & TCS Credit (along with any modifications) were received:

TDS (Tax Deducted at Source) Credit Received – This section applies only if you enter specific contracts with specific people (usually government bodies). As a Tax Deduction at the Source, the receiver (government) will deduct a set proportion of the transaction value. The deductor's GSTR-7 will auto-populate all the information here.

TCS (Tax Collected at Source) Credit Received –This section applies only to online retailers registered with an e-com operator. E-com operators are obligated to collect tax at source from sellers at the time of payment. This data will be auto-populated from the E-commerce operator's GSTR 8.

The format is as follows:

How Do I Access GSTR 2A?

Please follow the instructions below to view the GST 2A form:

Step 1: Go to the official GST website- www.gst.gov.in

Step 2: Log in using the required credentials

Step 3: On the dashboard, select "Services"

Step 4: Select "Returns" & then "Returns Dashboard"

Step 5: It will take you to the “File Returns” page, where you can enter the “Financial Year” & “Return Filing Period” & then click "Search"

Step 6: Then, under GSTR 2A, select the “View” option

Step 7: The GSTR 2A– Auto-drafted details page will then be displayed.

By selecting the relevant option in Step 6, you can also download this document for future reference.

What is the difference between GSTR 2A and 2B?

|

GSTR 2A |

GSTR 2B |

|

GSTR-2A is dynamic in nature, and it changes from day to day depending on when a vendor reports the documents. |

GSTR-2B is static in respect to one month. Due to this, change based on actions of the supplier can be taken later on. |

|

GSTR-2A doesn't include information or advice on what action a registered buyer should take. |

GSTR-2B Include an advisory next to each section indicating whether the ITC is qualified, disqualified, or reversed so that the taxpayer can take appropriate action on the same |

|

The maximum number of ITC entries displayed on the GST portal without having to download an excel file is 500. |

Under GSTR 2B, the maximum number of ITC entries displayed on the GST portal without having to download an excel file is 1000. |

What distinguishes GSTR 2A from GSTR-2?

|

GSTR 2A |

GSTR 2 |

|

GSTR 2A (goods & services tax returns) is a read-only doc generated automatically for informational purposes only. |

GSTR 2 can be changed, altered, and edited; however, GSTR 2A can't. |

|

Corrections can be made |

Corrections cannot be made |

Relationship and comparison between GSTR 3B and GSTR-2A?

- The GSTR 3B form is a monthly summary return filed by the taxpayer, while the GSTR 2A form is a GST Return that is automatically filled up and is only for informative purposes.

- GSTR 3B is a Goods and service tax return that contains a month's worth of data. As a result, the Input Tax Credit amount in Table 4(a) must match the GSTR 2A Form.

- If a discrepancy between GSTR 2A & GSTR 3B results i n an excess ITC being claimed, the extra ITC must be paid by the taxpayer, along with interest.

Reconciling Form GSTR-3B and Form GSTR-2B

It is critical to complete the Reconcile Form GSTR-3B with Form GSTR-2B because of the following reasons:

- A substantial number of taxpayers have received letters from the GST authorities requesting that they reconcile the ITC claimed in a self-declared summary return Form GSTR 3B with the auto-generated document GSTR 2A or GSTR-2B. Form GST ASMT– 10 is used to issue such notices. If the taxpayer doesn’t reply to these notices, they will be responsible for the discrepancy.

- Reconciliation guarantees that credit is only claimed for the tax that has been paid to the supplier in full.

- If the supplier has not reported the external supply in Form GSTR– 1, a notification to the supplier might be sent to ensure that the discrepancies are resolved.

- In addition, evaders claiming ITC based on bogus invoices have been sanctioned.

- Ensures that no bills are missed/recorded twice, and so on.

Non-reconciling Form GSTR-3B and Form GSTR-2B

For the following reasons, the details revealed in Form GSTR – 2A and Form GSTR – 3B may not match:

- IGST credit claimed on goods imported

- Credit for IGST on services imported

- ITC for goods & services received in the fiscal year 2020-21 but used in the fiscal year 2021-22.

- Credit for GST paid through the reverse charge system, and so on.

The figures will not reconcile in the circumstances indicated above if the supplier has not filed a corresponding Form GSTR – 1 or the ITC is being claimed at a later point.

Also Read: GSTR-4: Return Filing, Format, Eligibility & Rules

Conclusion

The government has enacted a number of rules and regulations in order to ensure honest taxation. The entire taxation procedure is two-fold in GST: one from the buyer's perspective and one from the seller's perspective. The returns' chain ensures that all the information submitted is accurate. For rechecking the transactions, various forms are generated. GSTR 2A (goods & services tax returns) is an auto-produced form generated in the buyer's account using the information from the seller's GSTR 1.