A cash flow statement is a type of financial statement that gives total information about all of the cash inflows a business makes from continuing activities and external investment sources. It also includes any cash outflows made within a specific period to cover investments and business expenses. On the other hand, a statement that includes the inflows and outflows of funds is known as a funds flow statement. It details the funding sources and how they were used during that specific period. As a result, you can investigate the causes of a change in a company's financial situation. This article will discuss the difference between cash flow and fund flow.

Did you know?

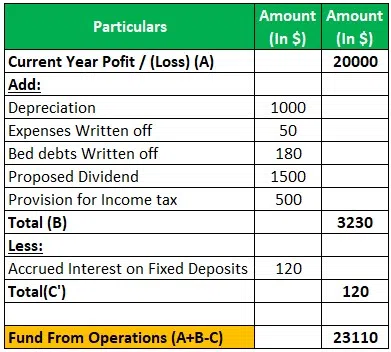

The cash flow statement will equal the balance sheet cash flow for that period.

What is a Cash Flow?

The inflow and outflow of cash and its equivalents are referred to as cash flow. Business operations, investments, and financing together facilitate cash flow. It establishes the status and availability of cash in a company. Understanding a company's cash flow is critical to understanding its financial situation, operations, and reported results. This analysis is used to estimate future cash flows. As a result, financial analysts plan short-term and long-term objectives as well as working capital and the ideal cash flow level based on such observation.

Also Read: What is the List of Accounting Standard

Types of Activities in a Cash Flow Statement

- Operating Activities: Operating activities incorporate the activities of a business in its regular course. Revenue from the sale of goods or services, dividends received by the company, interest, and other financial receipts are examples of inflows of cash. Payroll, overhead, taxes, and payments to suppliers and vendors are examples of outflows of cash.

- Investing Activities: Acquisition and disposal of non-current assets and other investments not covered under cash equivalents are included in cash flow from investing activities. The cash flows related to purchasing or selling real estate, investing in fixed deposits, mutual funds, stocks, plants, and equipment (PP&E), other non-current assets, and other financial assets are all considered forms of investment activity.

- Financing Activities: Any capital-related receipts and payments are considered to be financing operations. The capital raised through the issuance of long-term debt or equity is referred to as the inflow from finance. Cash inflows from the issuance of common stock, preferred stock, bonds, and different short- and long-term borrowings are also included. Shareholders and creditors are two important sources of funding. The repayment of loans, the redemption of bonds, the purchase of treasury shares, and dividend payments are all examples of money outflow. However, Indirect borrowing from accounts payable is categorised as cash flow from operating rather than financing activities.

Also Read: Fund Flow Statement - Meaning, Format And Examples

Steps for Preparing Cash Flow Statement

You must have both your income statement and balance sheet in hand to properly produce your cash flow statement. The stages of preparing a cash flow statement are described below:

- Step 1: Determination of Net Income:

By overviewing the income statement, you may determine your net income. The income statement includes a reflection of your operating activity. In essence, your net income is the result of your profits and total revenue over a specific period minus your losses and expenses over that same period. However, your net income and cash flow are not comparable.

- Step 2: Conversion of Net Income to Net Cash from Operating Activities

Due to the accrual method of accounting used in the income statement, adjustments are required to be reconciled with net income and net cash. When using the accrual method, a procedure is established for recognising revenue, which is frequently related to performing the task or rendering the service, and expenses are recorded whenever a commitment is made, as and when an agreement to pay is made.

This implies that the losses or gains listed in the income statement may not accurately reflect the amount of money that is in hand.

- Step 3: Calculation of Net Cashflow from Financing and Investing Activities:

It becomes considerably simpler to determine other cashflows after the determination of net cash flow from operating operations. Then, you must compute your net cash flow from financing and investing activities. No modifications are required for any of these categories; simply add your inflows and remove your outflows.

The next step is to add up the three values after you have a total for the net cash flows from all three activities. This will provide you with the total amount of cash flows that have increased (or decreased) over the specified period.

Also Read: Profit and Loss Account & Statement

What is a Fund Flow?

Fund Flow keeps track of a company's cash flow movement. It efficiently monitors the net inflows and outflows of cash from the financial system. A company's irregular expenses are also stated in Fund Flow.

The flow of money is necessary for a company's investment needs. The key difference between cash flow and fund flow is that cash flow facilitates investment decisions whereas fund flow does not show the true picture of the same.

To demonstrate movement and activity involving both long-term and short-term funds, fund flow statements provide the following information:

- How the money was raised (source of funds)

- How the money was utilised (application of funds)

Why is a Fund Flow Statement Prepared?

A balance sheet and a profit and loss statement are already included in a company's financial statements. Therefore, why is a fund flow statement even required?

The financial position of a firm is shown by its profit and loss statement and balance sheet, but these documents do not explain the causes of changes or variations in that position.

A balance sheet and profit and loss report will show two sets of numbers—the current and prior year—but they won't state why the numbers have changed. Therefore, a fund flow statement is necessary.

Also Read: Trial Balance: Rules Explained With Examples

Difference Between Cash Flow and Fund Flow

- One of the four financial statements that every investor analyzes to assess a company's financial health is the cash flow statement. The fund flow statement, on the other hand, is not a financial statement.

- To calculate the company's net cash flow after a certain period, the cash flow statement is produced. A fund flow statement is made to display the sources and expenditures of money over a given period as well as how this "change in the money" impacts the working capital of the business.

- The cash flow statement is produced using the cash system of accounting. On the other hand, the fund flow statement is produced using the accrual accounting system.

- Budgeting for cash involves using the cash flow statement. For capital budgeting, a fund flow statement is used.

Important Differences - Explained

|

Basis |

Cash Flow |

Fund Flow |

|

Definition |

Cash flow examines the cash inflows and outflows for a specific accounting period fund |

Fund flow assesses the sources and uses of the company's funds throughout a specific period. |

|

Purpose |

Cash flow demonstrates the company's liquidity, or if it has enough cash on hand to conduct its daily operations. |

Fund flow examines the financial status of the business to determine whether or not it is effectively managing its working capital. |

|

Result |

Cash flow determines the company's net cash position at the end of the accounting period fund |

Fund flow determines the changes in working capital over a specified time. |

|

Financial reporting |

According to GAAP guidelines, it is required that businesses include this statement for each period in their statement. |

Fund flow statements are not required to be reported by businesses, although they can be computed from the balance sheet. |

Conclusion:

A company informs creditors and investors when it releases financial statements. This information explains the financial health of the business. Investors can choose whether or not to invest in a firm using this information. Alternately, current investors will have the option to choose whether or not they wish to keep funding the business.

A firm's financial statements give investors and analysts a picture of all the business transactions that take place, where each transaction helps the company succeed. Because it tracks the cash generated by the business in three key ways—through operations, investments, and financing—the cash flow statement is the most understandable of all the financial statements.

Follow Khatabook for the latest updates, news blogs, and articles related to micro, small and medium businesses (MSMEs), business tips, income tax, GST, salary, and accounting.