Accounting is crucial to businesses because of a variety of reasons. The profit generations influence the viability and development of a company. But only the financial statements will be able to provide the required indicators to judge whether the amount earned covers the entire cost.

The basic concept may appear easy, but finding a source of income is extremely challenging. It is essential to implement a sound management technique to achieve success, and that also demands an effective accounting method within the business.

In this article, you'll discover the meaning of accounting, the importance of accounting, its purpose, its value in the business world and the various types of accounting.

Did You Know?

If we talk about the English word ‘accounting,’ it comes from a noun - account and everybody would think like this only. However, this word originated from the French word ‘acont.’ It meant account, terminal payment, or reckoning. Also, if we go deep, this old French term was generated from the Latin word ‘computus’, which meant ‘calculation.’

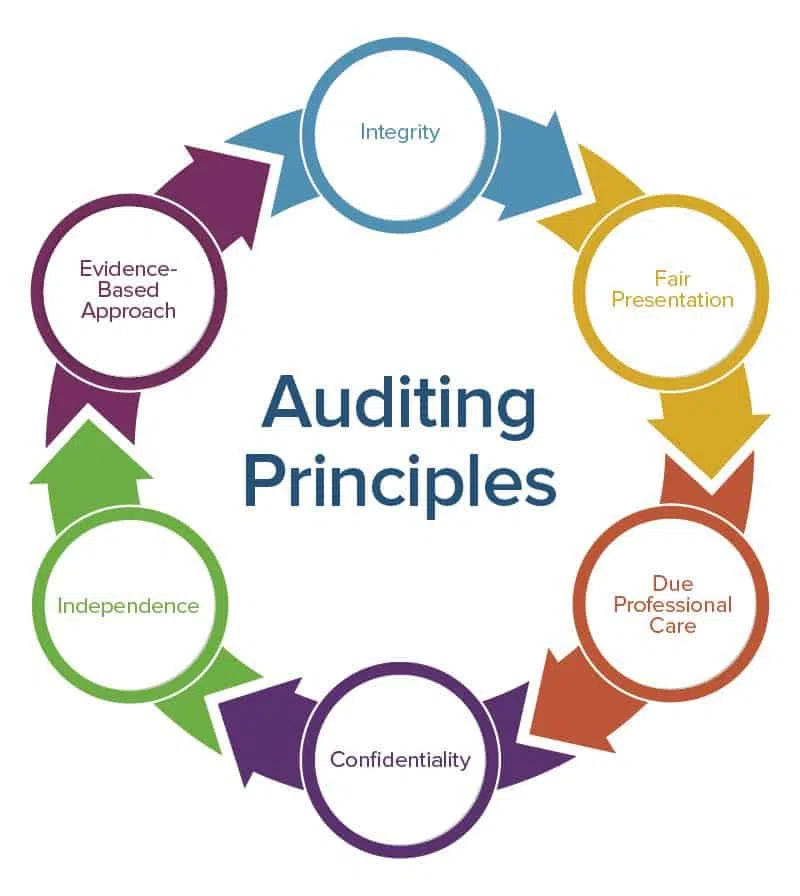

Also Read: Understanding Auditing, its Objectives, and Advantages

What Are the Types of Accounting?

There are various types of accounting documents, ranging from internal use only to reporting to regulatory agencies. Some are made for the public, while others are prepared for the benefit of customers, investors, or other parties interested in a business's performance.

To help you decide which one to use, here is an overview of the most common types of accounting documents. Read on to learn more about their purpose, differences and importance. Whether you plan to use an accounting document for internal purposes or prepare a public one, you'll find it here.

1. Financial Accounting

If we start learning about different types of accounting, financial niche comes first, and it is highly important. There are many reasons to understand financial accounting, including that it helps companies stay compliant with laws, attract investors and make informed decisions. However, if you’re a beginner, you can start by learning the basics of accounting.

Financial accounting includes creating the company's balance sheet, income statement and statement of cash flows. These statements are used to evaluate the health and performance of a company. Without these financial statements, there can be lawsuits or other problems.

Internal and external stakeholders use this type of accounting to gauge the health of a business. Shareholders and suppliers will want to see a financial report before investing, and brokers use this information to determine a company's stock value. Governmental and regulatory bodies also use financial reports to determine a business's legal and tax status.

However, financial accounting is not to be confused with managerial accounting, which internal managers use to make decisions within a business.

2. Cost Accounting

A company uses cost accounting to keep track of the costs associated with its operations and compare those costs to its revenue. The process helps determine how efficiently a company uses its resources.

Cost accounting uses a structured approach to calculating costs. This approach enables cost control and reduction by analysing transitions between the current accounting period and financial statements.

It also helps management to perform profitability analyses. It uses cost classifications based on products, activities and information needs. By combining these assessments, cost accounting helps organisations make more informed decisions.

In addition to the above benefits, cost accounting allows companies to create more accurate cost estimates.

3. Managerial Accounting

In addition to financial accounting, the managerial accounting involves the review of trends, including historical information and customer behaviour. It also involves calculating metrics, including cost and revenue, to determine how the company can best use its resources.

Managerial accounting also extends to other aspects of a business, including risk management, capacity evaluations and data analysis support for each business unit. In many cases, this information is used to determine the profitability of a particular product or service.

The managerial accounting functions are often stated qualitatively and are later translated to dollar value. Managerial accounting determines what variables will be used to measure a goal and plans how to quantify those measures.

4. Auditing

The process of auditing financial statements and records is crucial to the accuracy and reliability of the company's financial statements. In the past, financial statements of companies like Colgate were audited by PricewaterhouseCoopers LLP to ensure that internal control over financial reporting was effective.

In addition, this firm's audit of Colgate's finances included checking for errors. The results of this process are documented in the audit report. An auditor is a member of the middle management team of an organisation. His responsibility is to accurately portray the organisation's true financial status to its stakeholders. Although an accountant may manipulate financial results, he cannot lie.

An auditor is either internal or external to the organisation. Many companies opt for outside auditing firms. It is essential for an organisation's success to have an external auditor. This ensures that their accounting practices are accurate and consistent with the laws and regulations of their industry.

5. Accounting Information Systems

There are several different types of accounting information systems, including financial and management information systems. Historically, accounting systems were manually maintained in journals, but this method has become impractical with the growth of globalisation.

Accounting information systems are essential for the efficient management of retail resources and can serve as a comparative tool between businesses. They also assist management in determining useful trends and making necessary arrangements.

6. Tax Accounting

In the last five years, there have been numerous changes to tax accounting. Companies face more regulation than ever before concerning their income tax disclosures and account balances. A tax accountant may specialise in a particular niche within the field. However, they must be willing to expand their knowledge of various accounting techniques and software.

7. Forensic Accounting

Forensic accounting is a form of investigative accounting used in the legal arena to discover financial crimes. The process involves identifying, extracting, recording and reporting financial data and verifying the accuracy of the information.

The term forensic accounting was coined in 1946 by Maurice Peloubet, who was inspired by re-creating financial enigmas. Forensic accounting can be applied to many different situations, from uncovering hidden assets in divorce cases to handling civic matters.

Forensic accounting can also determine the economic impact of a breach of a non-disclosure or non-compete agreement. It plays an important role in investigating product liability and construction claims.

Also Read: What are the Limitations of Accounting?

Importance of Accounting

The Importance of accounting in Business is not limited to calculating financial numbers and reports. Accounting professionals have made significant contributions to history and the world at large. Here are the factors depicting the importance of accounting:

-

Helps to Create Budget

Creating a budget for your business is no small task, and it involves analysing costs, estimating revenue and projecting cash flow. Using an accounting system will give you real-time information on your business' finances.

As you begin to create your budget, remember to include all of your income and expenses and all expenses. This way, you will clearly understand your overall financial health. If you need to make adjustments, your accounting system can show you how to do so.

-

To Obtain Loans From Banks

To obtain a loan, a small business owner must demonstrate financial transparency. A good credit score will help lenders determine if a small business is reliable. Lenders will also look at cash flow and total minimum payments from all accounts and any debt the company has accumulated. When deciding what type of loan to grant, a small business owner should carefully consider the amount of accounting they need.

-

Decision Making

Managers often overlook the importance of accounting for decision-making and rely on factors that don't provide a sound foundation for their decisions. The goal of decision-making is to reduce uncertainty and risk by making the best possible decision.

It's imperative that decision-makers have the appropriate information to make the best choices, and a lack of accurate accounting information is a recipe for disaster. In a world where data is king, the importance of accounting information cannot be overstated.

-

Information to Stakeholders

An organisation has a wide range of stakeholders. These groups include shareholders, employees, creditors, government agencies and customers. All of them require different kinds of information. In addition to evaluating the performance of a business, stakeholders also seek to understand the organisation's strategies and tactics.

Financial statements are crucial for many stakeholders. They use these documents to evaluate a company's performance in the future. Therefore, they should be complete and accurate.

Reporting Profits

When a business is attempting to maximise its profitability, reporting profits is an important part of the process. This process reveals the total revenue and expenses that are directly related to the production of those sales.

Generally, direct expenses are broken down into two categories, cost of goods sold and sales. The cost of goods sold represents direct wholesale costs and is deducted from the total revenue to arrive at gross profit, and gross profit is the profit left over after all other expenses are paid.

Conclusion

After a thorough understanding of the most crucial accounting documents, the seller must know how to use them to achieve the greatest outcomes. Certain of these documents serve to prove sales, so they must be in top condition when authorities in charge ask for the documents.

Keep in mind that accounting documents can be altered at any time, and therefore, sellers should be aware of how to modify them to include the necessary information.

Now keep track of your cashflow and manage your incomes and expenses with ease by using the Cashbook app by Khatabook.