In economics, the long run is the conceptual period in which there are no fixed factors of production, and firms can adjust all inputs to desired levels. The long run is often contrasted with the short run, in which at least one factor of production is fixed.

In the long run, all costs are variable, and the firm can alter its scale of operations at will. The long run is, therefore, a period in which a firm can change its size and shape, build new factories, and hire new workers. In the long run, the firm's main goal is to minimise its average total cost.

The average total cost is the total cost divided by the quantity of output. It is the average cost of producing one unit of output. Marginal cost is the change in total cost that results from a one-unit increase in output. In the long run, marginal cost equals average total cost.

Did you know? In the long run, all costs are variable costs. This means that a firm can choose any level of output, and the only costs that will change are the variable costs. The long run is, therefore, a period in which a firm can change all of its inputs and outputs.

What Is Long Run Cost?

In economics, the long run is the conceptual period in which all factors of production and costs are variable. Long-run cost curves are important in microeconomics because they represent the least-cost method of production and provide important information about the efficiency of an organisation. The long run is also a period in which there are no fixed inputs, so a firm can change its plant size and the amount of labour it employs. In the long run, all costs are variable, which means that a firm can choose the optimal combination of inputs to minimise costs. The long run is an important concept because it allows firms to make decisions about how to use their resources best.

In the long run, a firm can choose the optimal combination of inputs to minimise costs. The long run is also a period in which there are no fixed inputs, so a firm can change its plant size and the amount of labour it employs.

Also Read: Cost Accounting vs Management Accounting

Types of Long Run Cost

There are 3 types of long run costs, which are as follows.

Long Run Total Cost

The long-run total cost (LRTC or LTC) is the total cost of production in the long run when all inputs are variable. This includes both the fixed and variable costs of production. The LRTC is important to understand because it helps firms determine the most efficient way to produce a good or service.

It also helps them understand how changes in inputs will affect their costs. In the long run, firms can change the scale of their production, which allows them to take advantage of economies of scale. This means that they can produce more output at a lower cost per unit. The LRTC also considers the opportunity cost of using a particular input. For example, if a firm uses the land to produce a good, the opportunity cost of that land is the value of the next best use of that land.

Long Run Average Cost

The average long-run cost (or LAC) measures a company's average cost to produce one unit of output over a long period. This metric is important to assess a company's competitiveness and is a key input in making pricing decisions.

The average long-run cost can be decomposed into two main components: fixed costs and variable costs. Fixed costs do not vary with output and include items such as rent and insurance, and variable costs are those costs that do vary with output and include items such as raw materials and labour. The average long-run cost is calculated by dividing fixed and variable costs by the number of output units.

Long Run Marginal Cost

In economics, marginal cost is the change in the total cost that arises when the quantity produced changes by one unit. So in the short run, some inputs are fixed so that the marginal cost will reflect the cost of the variable inputs. And in the long run, all inputs are variable, so the long run marginal cost (LRMC) includes the cost of any one additional unit of labour.

Marginal cost can be considered the cost of producing one additional unit of a good or service. The concept of marginal cost is important in microeconomics because it is used to make decisions about how much of a good or service to produce.

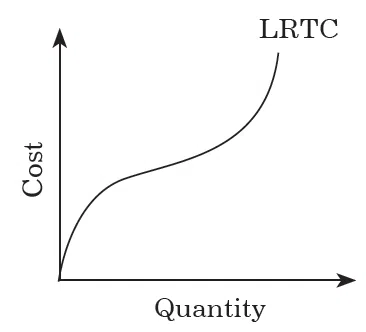

Long Run Total Cost Curves

A Long Run Total Cost Curve (LRTC) is a graphical representation of the relationship between a firm's long-run average cost (LRAC) and output levels. The LRTC is usually downward sloping, indicating that long-run average cost decreases as output increases. The LRTC can be used to analyse economies of scale, economies of scope, and the optimal scale of production.

Also Read: Matching Concept in Accounting: Benefits and Challenges

Long Run Average Cost Curves

Long-run average cost curves (LAC) show how much it costs a firm to produce a given output level as the number of units of input increases. The LAC curve is U-shaped, which means that as the number of units of input increases, the average cost falls and then rises. The fall in average cost is due to economies of scale, while the rise is due to diminishing returns. Diminishing returns occur when the marginal product of an input (e.g. labour) starts to fall as the level of that input increases. This happens because, at some point, the extra workers are not as productive as the earlier workers.

Long Run Marginal Cost Curves

A long-run marginal cost curve (LRMCC) is a graphical representation of how the marginal cost of production changes as the scale of production increases. The LRMCC is a key tool used by economists to analyse firms’ production decisions and to understand how industries evolve. The LRMCC can be used to analyse how a firm’s costs change as it expands its scale of production and how this affects its competitiveness in the long run. The LRMCC can also be used to understand how an industry’s structure changes as new firms enter and exit the market.

Also Read: What Is Vouching in Accounting?

Conclusion:

As a business owner, it is important to understand your long-run costs in order to make informed decisions about your pricing and output. Total cost is the sum of all your costs, including fixed and variable costs. The average cost is your total cost divided by the number of units you produce, and marginal cost is the additional cost of producing one more unit.

In the long run, all costs are variable, and you can adjust your output to meet demand. To maximise profits, you should produce at the level where marginal cost equals marginal revenue.

Follow Khatabook for the latest updates, news blogs, and articles related to micro, small and medium businesses (MSMEs), business tips, income tax, GST, salary, and accounting.